Transfer pricing in Singapore

Tax factsAll related party transactions should be conducted at arm's length, ie as if parties were unrelated.

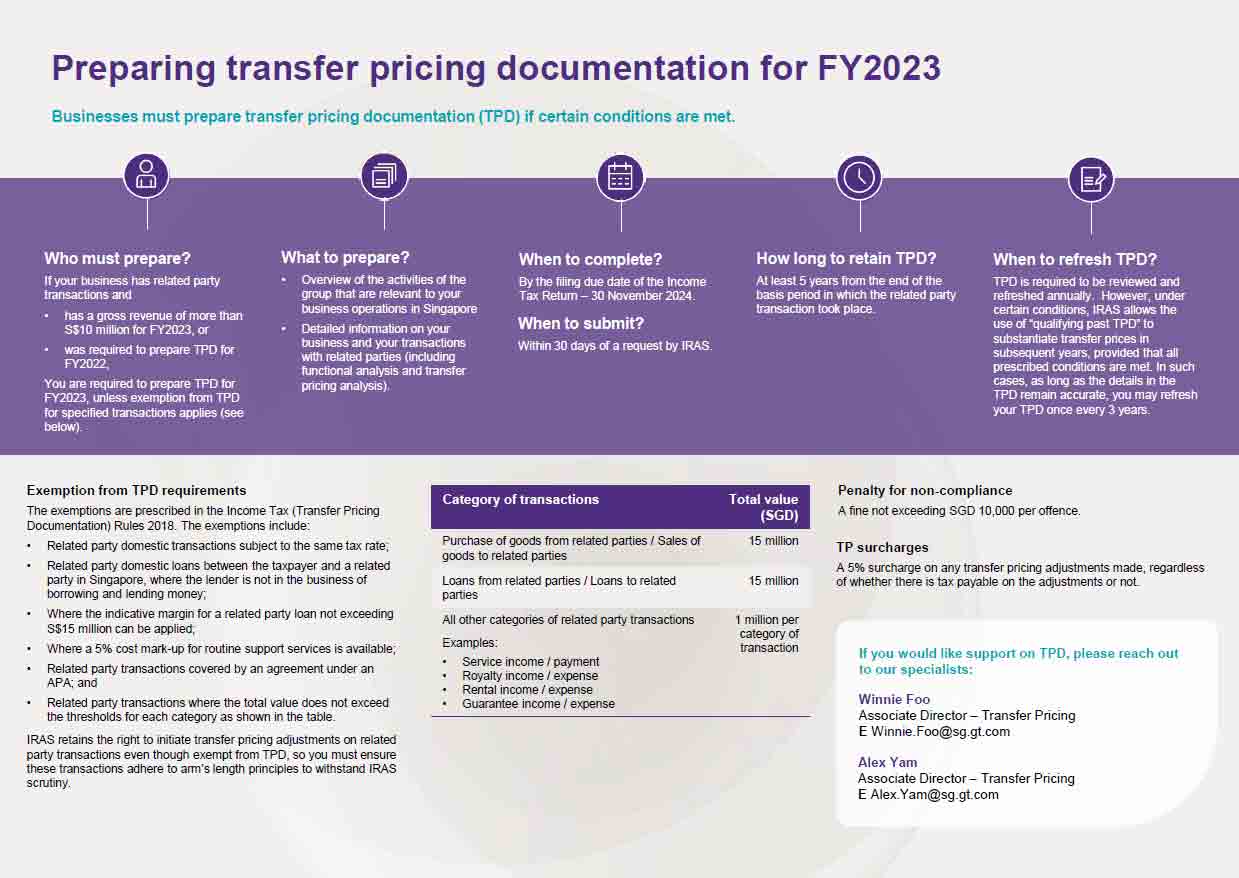

From the year of assessment (YA) 2019 onwards, unless exemption from TPD for specified transactions applies (see further on point 4), Singapore taxpayers must prepare TPD when either of the following two conditions are met:

TPD is crucial for taxpayers to demonstrate that their related party transactions are conducted at arm’s length. Together with inter-company agreements, TPD serves as the primary defence during transfer pricing audits.

If the taxpayer is unable to show with their TPD that their transfer pricing is at arm’s length or they do not have TPD to substantiate their transfer prices, it can lead to several adverse consequences:

These consequences have the potential to disrupt business operations and damage a company’s reputation.

Taxpayers are advised to adhere to the content requirements outlined in the TPD Rules when preparing their TPD, which include:

Taxpayers with gross revenue from a trade or business not exceeding SGD 10 million for the relevant basis period, or when not specifically requested by IRAS, are generally exempt from preparing TPD.

However, if taxpayers who are required to prepare TPD experience declining revenue such that their gross revenue is consistently below SGD 10 million, they will be exempted from preparing TPD if their gross revenue is not more than SGD 10 million for that basis period and the immediate two preceding basis periods.

For taxpayers who are required to prepare TPD under Section 34F of the ITA but are not eligible for the gross revenue exemption, a secondary check is applied to assess if TPD can be exempted for specific transactions under the TPD Rules. These specified transactions include:

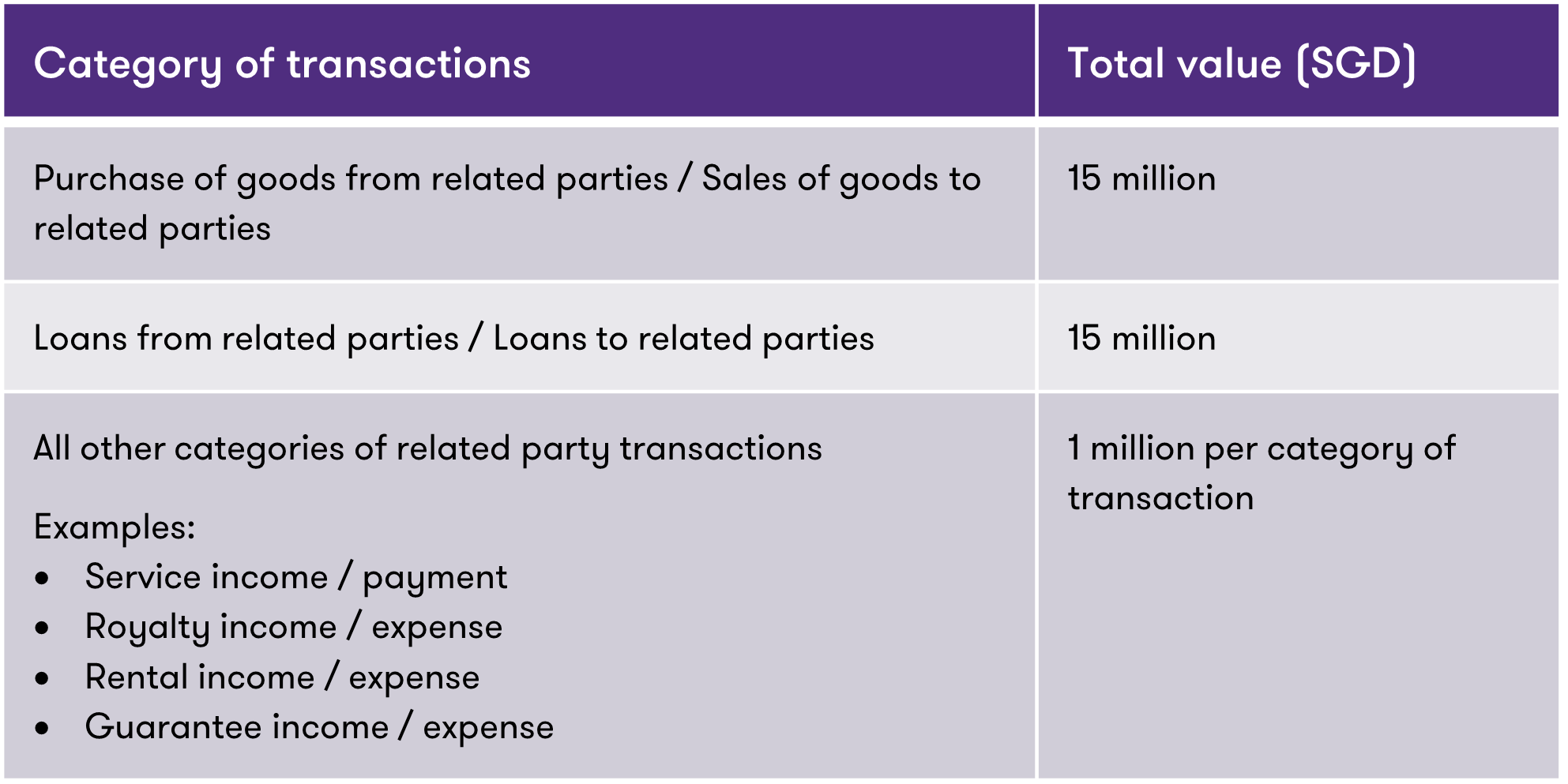

a. Related party domestic transactions subject to the same tax rate;

b. Related party domestic loans between the taxpayer and a related party in Singapore, where the lender is not in the business of borrowing and lending money;

c. Where the indicative margin can be applied for a related party loan not exceeding SGD 15 million;

d. Where a 5% cost mark-up for routine support services is available;

e. Related party transactions covered by an agreement under an APA; or

f. Where the total value or amount of all the related party transactions (excluding those mentioned in points (a) to (d) above) in the basis period concerned do not exceed the thresholds for each category as shown in the following table:

TPD must be completed by the filing due date of the Income Tax Return.

Taxpayers are not required to submit their TPD when filing a tax return. However, they must submit their TPD within 30 days of a request from IRAS.

Taxpayers are expected to review and refresh their TPD annually.

However, under certain conditions, IRAS allows the use of “qualifying past TPD” to substantiate transfer prices in subsequent years. To be regarded as “qualifying past TPD”, the TPD must meet the following criteria:

Taxpayers should retain TPD for at least 5 years from the end of the basis period in which the related party transaction took place.

Non-compliance with the TPD requirements may result in penalties not exceeding SGD 10,000 per offence. These offences include:

In cases where IRAS initiates transfer pricing adjustments, a 5% surcharge is imposed on the adjustments, regardless of whether there is tax payable on the adjustments made.

IRAS retains the right to initiate transfer pricing adjustments on related party transactions exempt from TPD, so taxpayers must ensure these transactions adhere to arm’s length principles to withstand IRAS scrutiny.

Under certain circumstances, IRAS may grant a full or partial remission of the surcharge. These circumstances include co-operative and responsive behaviour of taxpayers, maintenance of contemporaneous TPD and good tax compliance records.

We encourage taxpayers to take a proactive approach to managing their transfer pricing risks by preparing contemporaneous TPD. During the preparation of such documentation, there is often an opportunity to identify further risk mitigation strategies. By proactively managing their transfer pricing risks and ensuring proper documentation, taxpayers can mitigate these risks and maintain good tax compliance.

All related party transactions should be conducted at arm's length, ie as if parties were unrelated.

Transfer pricing regulations by the Organisation for Economic Cooperation and Development (OECD) and Singapore have specific provisions to talk about intercompany service transactions. This article delves into what Singapore taxpayers need to know about service transactions under these regulations and highlights typical mistakes businesses may make.

The release of the 7th edition of the Singapore Transfer Pricing Guidelines on 14 June 2024 signifies a substantial advancement in the efforts of the Inland Revenue Authority of Singapore (IRAS) to enhance clarity and rigour in the Singapore transfer pricing (TP) landscape. This edition introduces both minor and major updates across nine sections of the Guidelines, reflecting an evolving and more sophisticated approach to TP analysis and compliance with the arm’s length principle.

Subscribe for timely technical updates and keep on the pulse with industry developments