Lease Accounting

Services

FRS 116 – Leases

FRS 116 - an introduction

The Financial Accounting Standards Board (FASB), International Accounting Standards Board (IASB) and the Accounting Standards Council (ASC) of Singapore have embarked on ushering in a new era of lease accounting. A new leasing standard is expected to bring about a paradigm shift in the accounting and recognition of leases by lessees.

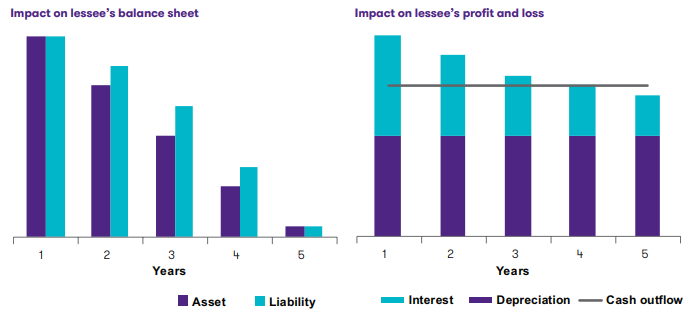

In June 2016, ASC issued FRS 116, Leases with effect from 01 January 2019. For investors and analysts, FRS 116 on Leases will enhance the comparability of balance sheets of companies that borrow to buy assets with those that lease assets. For lessees’ balance sheet, while eliminating the classification of a lease as operating or finance lease, FRS 116 will result in an increase in assets (via a right-of-use assets concept) and corresponding increase in financial liabilities. On the P&L side, the straight-lined lease expense will be replaced by a depreciation charge and interest expense, resulting in a year-on-year fluctuation in profitability. It is expected that FRS 116 will facilitate better capital allocation by enabling better credit and investment decision-making by both investors and companies.

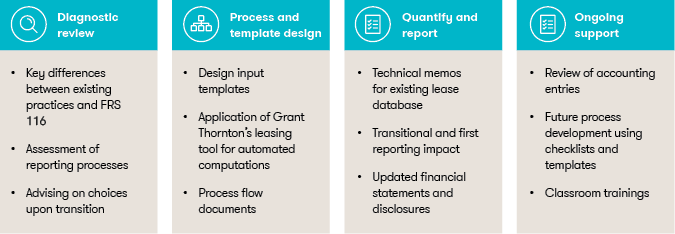

Grant Thornton differentiators: FRS 116 implementation

We handhold in transition process for first time reporting, along with assistance in preparation and designing of disclosure and computational templates, to achieve smooth transition to the new lease accounting model under FRS 116.

Grant Thornton understands the priorities and thus offers a four-stage solution: