What is Pillar 1 in BEPS 2.0

Pillar 1 is intended to reallocate profits and related taxing rights from certain jurisdictions where multinational enterprises (MNEs) have physical substance, to other countries where they have a customer base, regardless of whether they have a physical presence in that second jurisdiction.

To determine the profit allocation to a particular market jurisdiction, Pillar 1 uses two formulas:

- Amount A – This applies to MNEs with consolidated revenue exceeding EUR 20 billion and profitability greater than 10% of revenues. It reallocates a portion of the MNE’s profit to market jurisdictions that satisfy the quantitative nexus test.

- Amount B – This is a fixed remuneration for basic marketing and distribution activities (with no revenue threshold).

Key Summary of Pillar 1 - Amount B report

On 19 February 2024, the OECD published a report on Amount B outlining the process for simplifying and streamlining the application of the arm’s length principle for in-country baseline marketing and distribution activities. This is meant to assist low-capacity jurisdictions1 that often struggle with limited resources and data availability for determining an arm’s length return on those types of activities. The report will form part of the Annexes of the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2022 (“OECD TP Guidelines”).

The Inclusive Framework2 (“IF”) is still working on additional qualitative scoping criteria to identify distributors performing non-baseline activities for the purpose of a simplified and streamlined approach, the design elements (i.e., pricing matrix, operating expense cross-check, and data availability mechanism) and the list of low-capacity jurisdictions. This is supposed to be finalised by 31 March 2024 but there has been no updates.

Countries may opt to apply the approach for in-scope transactions from 1 January 2025. Consistent with other optional approaches in the OECD TP Guidelines, it is non-binding on jurisdictions.

Transactions that are in-scope of Amount B

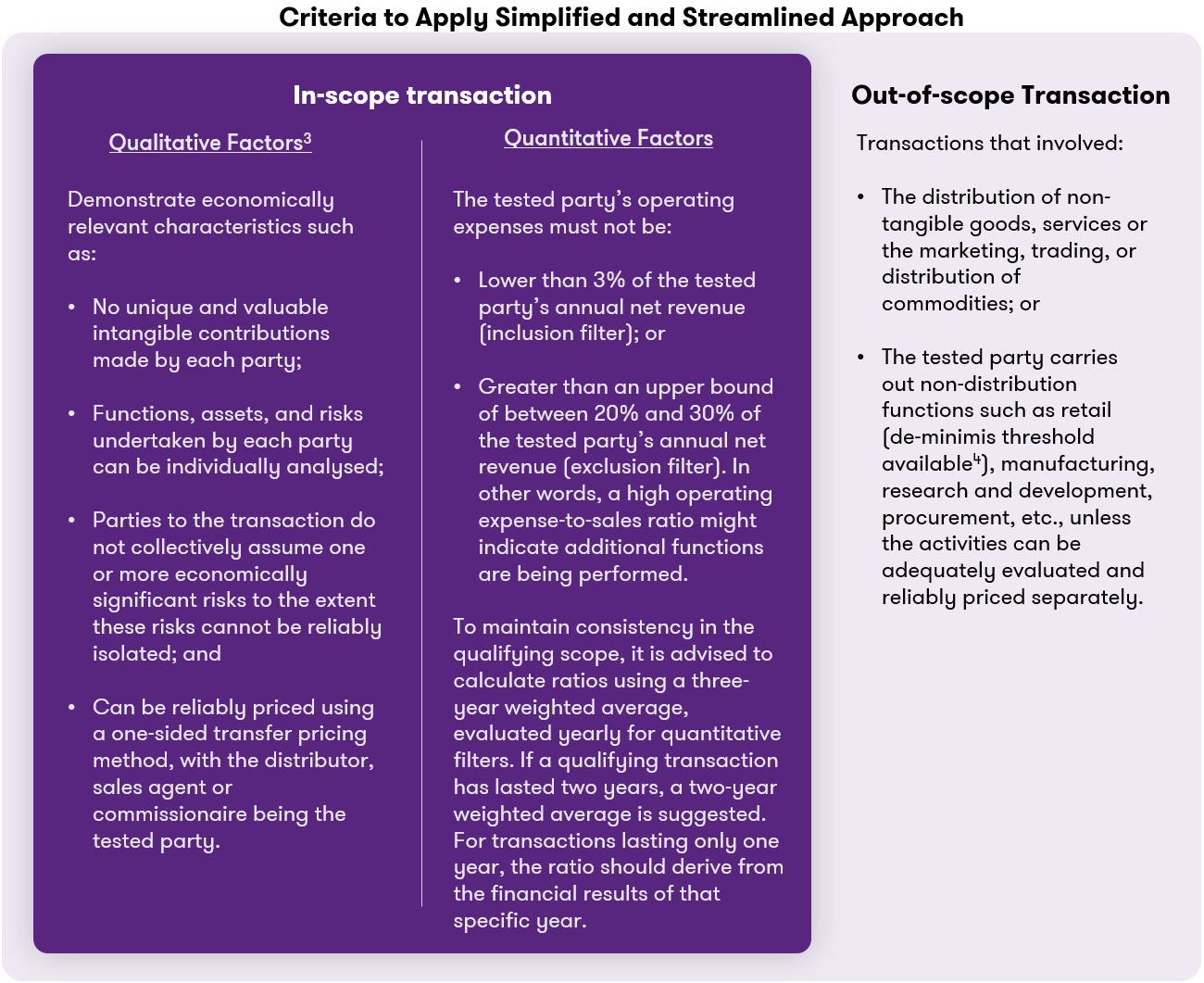

Qualifying transactions for the simplified and streamlined approach are:

- Buy-sell marketing and distribution transactions: These involve a distributor purchasing goods from associated enterprise(s) for wholesale distribution to unrelated parties; and

- Sales agency and commissionaire transactions: These involve the remuneration of the sales agent or commissionaire to one or more associated enterprises’ wholesale distribution of goods to unrelated parties.

The assessment criteria are outlined below:![]()

Application of the simplified and streamlined approach

The transactional net margin method is considered the most suitable method for pricing in-scope transactions. Nonetheless, the comparable uncontrolled price method may be used if internal data is available and reliable.

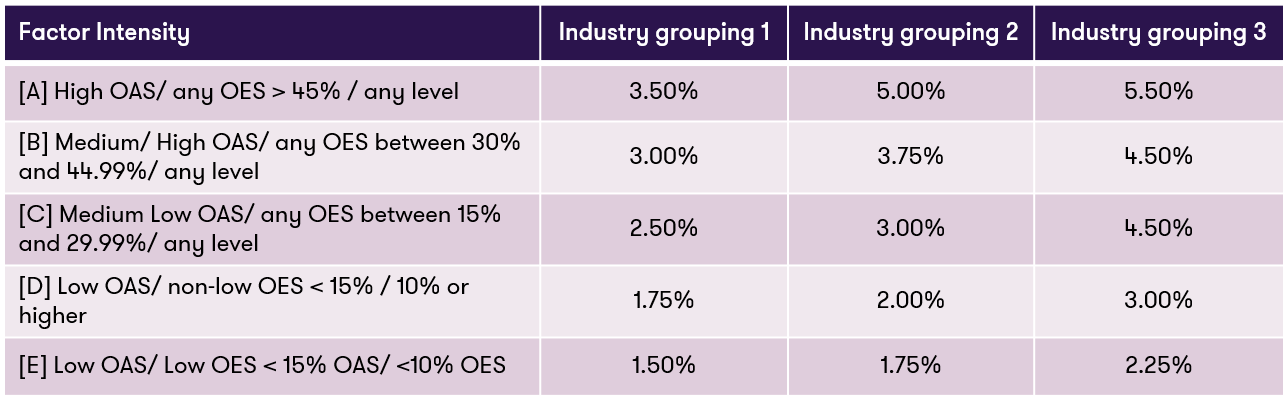

Return on Sales (“ROS”) has been selected as the net profit indicator for pricing the in-scope transactions. Businesses will apply and test the actual outcome of the in-scope transactions on an ex-post basis against the pricing matrix (plus or minus 0.5%) established on three industry groups and five categories of operating asset (“OAS”) and operating expense (“OES”) intensities as illustrated below: ![]() An operating expense cross-check acts as a corroborative guardrail to test whether the ROS provided using the pricing matrix is appropriate, or whether additional adjustments are required. If the ROS determined under the pricing matrix falls outside the following pre-defined operating expense cap and collar range, the ROS will be adjusted to the nearest edge of the range.

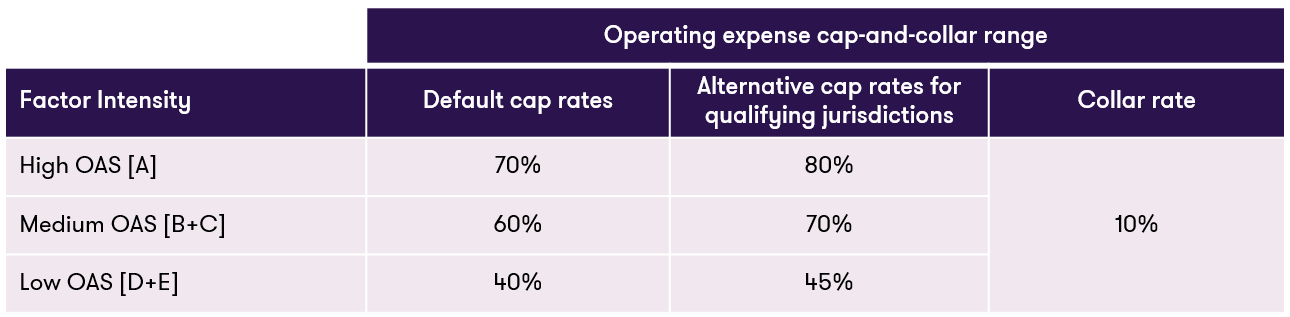

An operating expense cross-check acts as a corroborative guardrail to test whether the ROS provided using the pricing matrix is appropriate, or whether additional adjustments are required. If the ROS determined under the pricing matrix falls outside the following pre-defined operating expense cap and collar range, the ROS will be adjusted to the nearest edge of the range. ![]() An additional adjustment is also required based on the in-scope distributors operating jurisdictions’ sovereign credit rating.

An additional adjustment is also required based on the in-scope distributors operating jurisdictions’ sovereign credit rating.

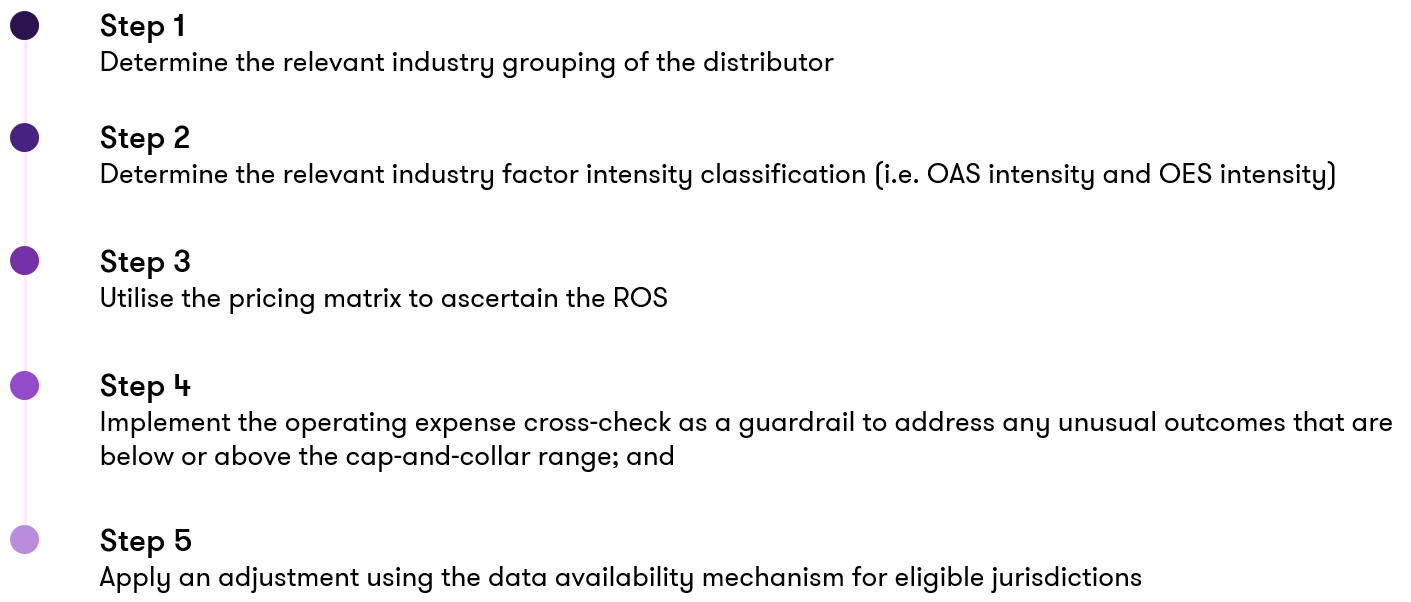

In summary, the processes for determining the approximate arm’s length ROS for an in-scope distributor are as below:

![]()

Key takeaways from the Amount B report

It is a welcome development to see the IF trying to alleviate administrative burdens, cut compliance costs, and enhance tax certainty for businesses. However, there is no unanimous decision among IF members that this typically complicated OECD approach will achieve those objectives. As a result, the simplifying and streamlining approach remains elective and non-binding. The final consensus at this point remains unclear. However, we understand already that New Zealand has voted with its feet and said it will not be applying the new option.

Businesses who wish to adopt the approach should first consider the following:

- The approach is still evolving. Additional clarity is required regarding the qualitative factors, such as the criteria to identify distributors performing non-baseline activities, the design elements and the list of low-capacity jurisdictions.

- The approach mainly applies to MNEs engaged in the wholesale trade of tangible goods who employ routine or limited-risk distributors. However, categorising a distributor as "routine" or "limited risk" for transfer pricing purposes does not automatically classify it as a baseline distributor under Amount B, and vice versa.

- The application may not necessarily be simpler than the traditional method of conducting a benchmarking analysis to establish the arm’s length range for baseline distribution activities. The simplified approach mandates a precise definition of the qualifying transaction to verify its applicability, followed by comprehensive quantitative analysis to determine the suitable return garnered by the baseline distributor.

- It will be interesting to see how various jurisdictions choose to implement the approach. We may end up with a divided world, in which some will adopt the Amount B approach and others will not. The outcome determined under the simplified and streamlined approach by one jurisdiction does not bind the counter-party jurisdiction. This aspect will undoubtedly complicate the process, making it a less appealing initiative than it appears. That is unless a majority of jurisdictions opt for its application, ensuring consistency among tax authorities.

[1] The list of qualifying jurisdictions will be fixed prospectively based on those qualifying criteria, published and updated every 5 years on the OECD website.

[2] Consists of 145 countries as of 15 November 2023.

[3] An accurate definition of the functions performed, assets employed, and risks assumed is required to be undertaken in accordance with Chapter I of the OECD TP Guidelines.

[4] Three-year weighted average net retail revenue (excluding distribution of digital goods, commodities, and services) divided by three-year weighted average net revenues > 20%.

An operating expense cross-check acts as a corroborative guardrail to test whether the ROS provided using the pricing matrix is appropriate, or whether additional adjustments are required. If the ROS determined under the pricing matrix falls outside the following pre-defined operating expense cap and collar range, the ROS will be adjusted to the nearest edge of the range.

An operating expense cross-check acts as a corroborative guardrail to test whether the ROS provided using the pricing matrix is appropriate, or whether additional adjustments are required. If the ROS determined under the pricing matrix falls outside the following pre-defined operating expense cap and collar range, the ROS will be adjusted to the nearest edge of the range.  An additional adjustment is also required based on the in-scope distributors operating jurisdictions’ sovereign credit rating.

An additional adjustment is also required based on the in-scope distributors operating jurisdictions’ sovereign credit rating.