The Ministry of Finance recently released the draft Goods and Services Tax (Amendment) Bill 2019 for public consultation which included a proposed amendment to the GST treatment of digital payment tokens. Around the same time, the Inland Revenue Authority of Singapore (“IRAS”) released a draft “e-Tax Guide” outlining the proposed changes on the GST treatment of digital Payment Tokens, which closed for comments on 26 July 2019.

The changes are aimed at trying to align the GST treatment with the growing consensus of indirect tax treatments in other jurisdictions such as Australia, the European Union, Japan and Switzerland ensuring there is no competitive disadvantage for businesses trading in Singapore.

What are Digital Payment Tokens?

“A digital payment token refers to any cryptographically-secured digital representation of value that can be transferred, stored or traded electronically”

Under the draft legislation, a digital payment token must have the following characteristics:

- It is expressed as a unit

- It is fungible

- It is not denominated in, or pegged, to any currency

- It can be transferred, stored or traded electronically

- It is intended to be a medium of exchange accepted by the public, or a section of the public, without any substantial restrictions on its uses as consideration

The IRAS’ draft e-tax guide gives examples of digital payment tokens which include Bitcoin, Ethereum, Litecoin, Dash, Monero, Ripple and Zcash.

What are the proposed changes and their implications?

Under current rules, the supply of virtual currencies and the use of virtual currencies to pay for goods and services are treated as taxable supplies of services. This would generally give rise to double taxation issues.

The proposed changes which are to take effect from 1 January 2020 are two-fold and are summarised as follows:

- Use of digital currency as a payment for goods/services is not a supply for GST purposes

This should positively impact businesses using digital payment tokens to pay for goods or services because they will no longer be required to account for output tax on the value of the digital payment tokens transferred. The transfer can simply be disregarded for GST purposes.

- Exchange of digital currency for a “fiat” currency or any digital token is exempt from GST

The implications of this change are more complex and far reaching. They include, but are not limited to the following:

- The issue of digital payment tokens (e.g. initial coin offerings) will be exempt from GST (potentially zero-rated if the issue is to overseas customers.) Such businesses will not be entitled to register for GST in Singapore and thus all input tax incurred on costs will be irrecoverable, increasing their cost base. While the draft e-tax guide is silent on the liability for GST registration if the issue is to overseas customers or made on an overseas exchange, which would be zero-rated supplies, we assume the normal rules for voluntary registration would apply to allow the GST registration, where appropriate.

- Businesses who exchange digital payment tokens are likely to become partially exempt (make a mixture of exempt and taxable supplies.) Input tax incurred on exempt supplies is not recoverable and such businesses will need to attribute and apportion input tax incurred on costs, again increasing their cost base.

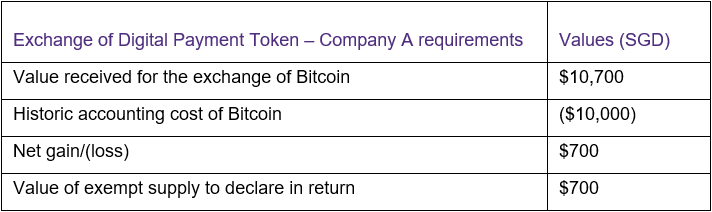

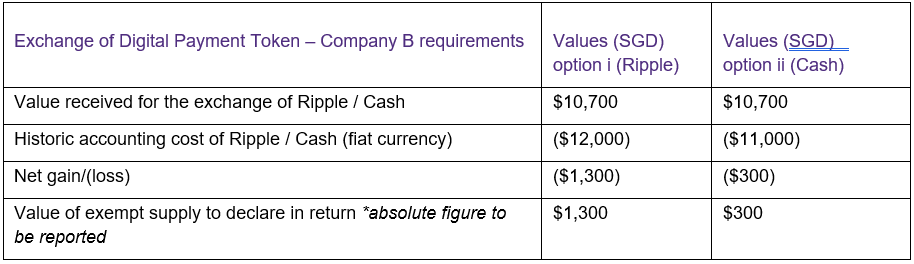

Example: Post 1 Jan 2020 Exchange of Digital Payment Token

![imagek3kne.png]()

![imagegm6k7.png]()

![imagepnxse.png]()

For more information, contact our expert Jeremy O'Neill.