Entity X has a non-amortising loan of CU 10,000,000 from the bank. Interest is set at a fixed rate of 5%, which is payable quarterly. Maturity date is 31 December 2025.

On 1 July 2020 the bank agrees to waive interest for two quarterly periods from 1 July 2020 to 31 December 2020. In addition, the contractual rate of interest is increased to 8% starting 1 January 2021.

As part of the modification, the entity pays a CU 150,000 arrangement fee to the bank and a CU 50,000 professional service fee to its lawyers.

Analysis

The entity carries out the 10% test:

- the net present value of the future revised cash flows, discounted at the original EIR inclusive of fees paid to the lender is CU 10,990,426 plus CU 150,000 which is equal to CU 11,140,426.

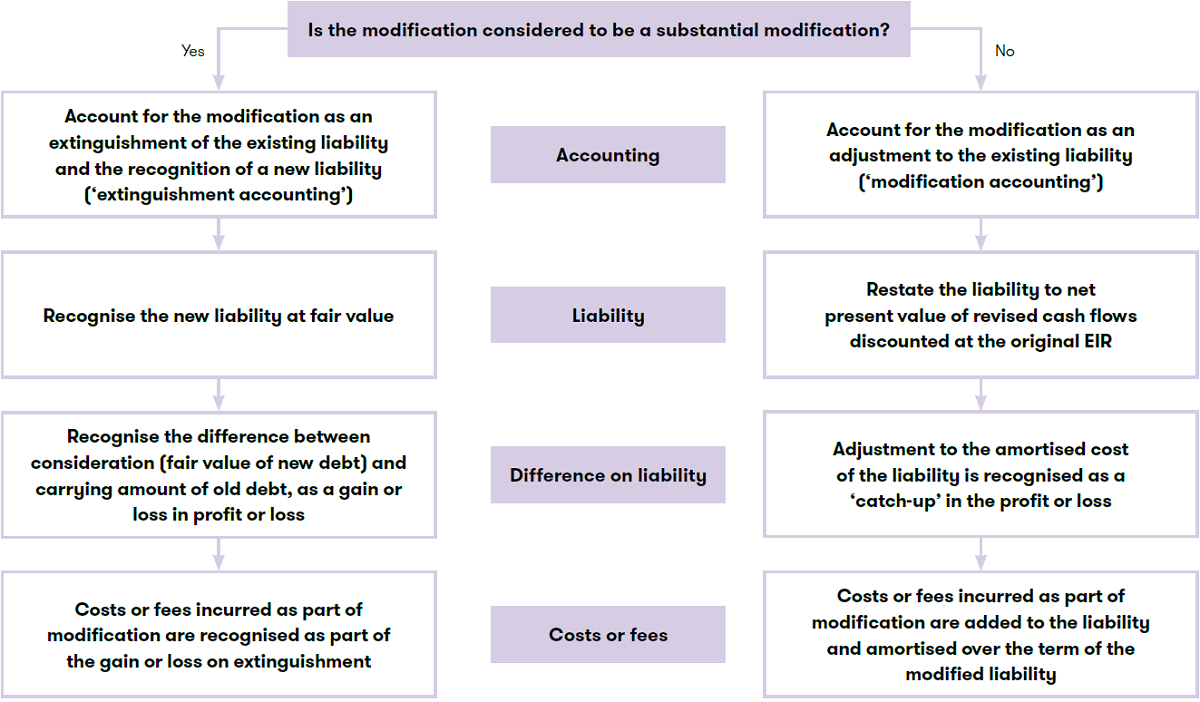

- for the purposes of the 10% test this is compared to CU 10,000,000 giving an 11.4% difference. This is more than 10%, so the loan modification (waiver of 6 months of interest and subsequent increase of the contractual interest rate) is considered to be a substantial modification.

- the legal fees are judged not to be incremental to the issue of the new debt, as they include elements relating to advice on the pre-existing debt’s contractual terms.

The initial liability has to be extinguished and a new liability recognised at its fair value as of the date of the modification. Given the market rate of interest is 12% for a comparable liability, the fair value of the liability amounts to CU 8,122,994. The difference of CU 1,877,006 between this initial fair value of the new liability and the carrying amount of the liability derecognised (CU 10,000,000) is recognised as a gain upon extinguishment. All fees incurred (CU 200,000) are immediately expensed, thus reducing the amount of the net gain upon extinguishment to CU 1,677,006.

Therefore, the following journal entries should be recorded:

| Journal: |

CU |

CU |

| Dr Existing liability |

10,000,000 |

|

| Cr New liability |

|

8,122,994 |

| Cr Cash (bank and legal fees paid) |

|

200,000 |

| Cr Profit or loss (gain on extinguishment) |

|

1,667,006 |